11 November 2016

Our forecast last week indicated an expected 53c/l drop for petrol and a 37c/l drop for diesel, both with a margin of error of 20c/l. The favourable oil price and stable rand since then have increased the over recovery for petrol to 44c/l from 12c/l and diesel to an over recovery of 25c/l from an under recovery of 11c/l.

Our current forecast indicates an expected drop in December of 67c/l and 50c/l for petrol and diesel respectively. Due to fewer days remaining in the cycle, the margin of error in our forecast has reduced to +/- 13c/l.

The Rand weakened sharply yesterday afternoon, as the market absorbed the consequences of a Trump presidency. This move happened too late in the day to affect yesterday’s data point, so it has not yet impacted expectations. However, even if the Rand remains at current levels (14.30) for the remainder of the pricing cycle, we still expect petrol prices to drop by 44c/l and diesel 27c/l.

The table below indictaes our current forecasts

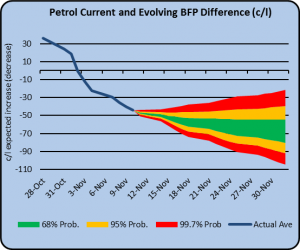

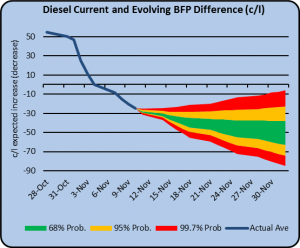

The graphs above show the current average price difference between market rates and the current Basic Fuel Price (BFP) and varying ranges of future outcomes based on 1,2 and 3 standard deviations.

They are based on market data from 28 Oct – 10 Nov, comprising 10 of the 25 data points in the current cycle, and 10,000 possible price scenarios for the remaining 15 business days.

The forecasts are formulated based on actual historical moves, using specifically designed forecasting tools, and not on subjective market predictions for the oil price or the USD/ZAR exchange rate.

As with any statistical forecast, as more data becomes available, the forecast will become increasingly accurate, and the range of possible price changes will reduce.

All data is sourced from data published by CEF, including historical data from March 2014. (http://www.cefgroup.co.za/petrol-price/)

We will update these forecasts weekly.

Recent Comments